Super Micro Computer (SMCI) had a phenomenal beginning this year, with shares soaring over four times their value from January to mid-March. This impressive rise made Super Micro a candidate for inclusion in the S&P 500, leading to its addition to the index on March 18, 2024. Looking back, that would’ve been an opportune moment to either cash out or short the stock, as the share price has plummeted by over 50% since then.

A significant factor in this decline has been the report from Hindenburg Research, which raised serious concerns regarding the company’s financial practices. Given these allegations and Super Micro’s overall fundamentals, I maintain a neutral outlook on the stock.

Hindenburg Raises Concerns Regarding Super Micro

The Hindenburg report is a primary reason for my neutral stance instead of a bullish one on SMCI stock. It has caused hesitation among numerous analysts and investors in the AI sector.

The allegations presented are stark. Hindenburg claims that Super Micro engaged in accounting irregularities, including “sibling self-dealing and sanction evasion.” Those who find these claims implausible may recall that the SEC had previously charged Super Micro with significant accounting violations back in August 2020. Moreover, Hindenburg suggested that many individuals involved in past accounting misconduct are back on Super Micro’s team.

Hindenburg’s researchers interviewed several sales representatives and employees of Super Micro as part of their investigation. The fact that Super Micro postponed its 10-K filing to review internal controls shortly after Hindenburg made its concerns public is troublesome, even if coincidental. Historically, Super Micro had difficulty with financial filing in 2018, resulting in a temporary delisting from Nasdaq.

Earlier this month, Super Micro officially denied the allegations, with CEO Charles Liang stating that Hindenburg’s report featured “misleading presentations of information.” Since then, no further statements have been released by Super Micro.

The Growth of Artificial Intelligence is Indisputable

Super Micro’s involvement in the rapidly expanding AI sector is one of the few reasons I remain neutral rather than bearish on SMCI stock. The exciting opportunities for the company’s business counterbalance the serious nature of the allegations from Hindenburg.

Determining what’s fact versus what’s fiction is challenging, but it is generally accepted that the AI industry presents substantial growth potential. Nvidia (NVDA) has reported triple-digit year-over-year revenue increases for several quarters. Other tech giants are incorporating AI into their main operations, yielding impressive results for their shareholders. For instance, Alphabet (GOOGL) experienced a 28.8% year-over-year rise in cloud revenue as many companies hurried to develop their own AI solutions.

The artificial intelligence industry is forecasted to maintain a 19.3% compounded annual growth rate from now until 2034, according to Precedence Research. The AI market should continue to thrive, positively impacting Super Micro. The firm is likely to gain from Nvidia’s expansion, which is reflected in its outstanding revenue and net income growth during Nvidia’s rise over the past several quarters. However, we remain uncertain about the integrity of those figures, especially in light of Hindenburg’s allegations.

Super Micro Displays Strong Financials at First Glance

While the claims from Hindenburg cannot be dismissed, it’s still valuable to evaluate Super Micro’s prior quarterly performance. Shares were on a downward trajectory even before the Hindenburg report emerged. In March 2024, I noted that SMCI stock was at risk, although I believed the shares represented an excellent buying opportunity in late summer until Hindenburg clouded that optimism.

In its most recent quarter, Super Micro reported net sales of $5.31 billion, reflecting a remarkable 143% increase year-over-year. Likewise, net income surged 82% year-over-year, hitting $353 million. At that time, my main concern was Super Micro’s declining net profit margin. The stock currently trades at a trailing P/E ratio of 20x, which appears adequate to absorb any further margin erosion. SMCI stock boasts an incredibly low forward P/E ratio of 13.6x, but due to recent challenges (the Hindenburg report and DOJ inquiry), investors seem hesitant to elevate the valuation multiple.

There is no concrete evidence yet that Super Micro engaged in any misconduct as alleged by Hindenburg, but their report has undoubtedly tarnished the stock’s reputation. I believe Super Micro would have likely outperformed its fiscal 2023 expectations even without any alleged improprieties.

The Department of Justice Is Investigating Super Micro Computer

The ongoing Super Micro controversy escalated on September 26, when it was revealed that the U.S. Department of Justice is now investigating the company. SMCI stock dropped an additional 12% following this announcement, with shares trading at less than one-third of their peak value in March. There are high risks/rewards associated with the stock at this juncture; however, the heightened risks have kept me on the sidelines with a neutral rating.

On September 27, Super Micro shares rebounded by over 4%, signaling that many investors see long-term potential in the business despite the ongoing uncertainty.

Should You Buy Super Micro Stock?

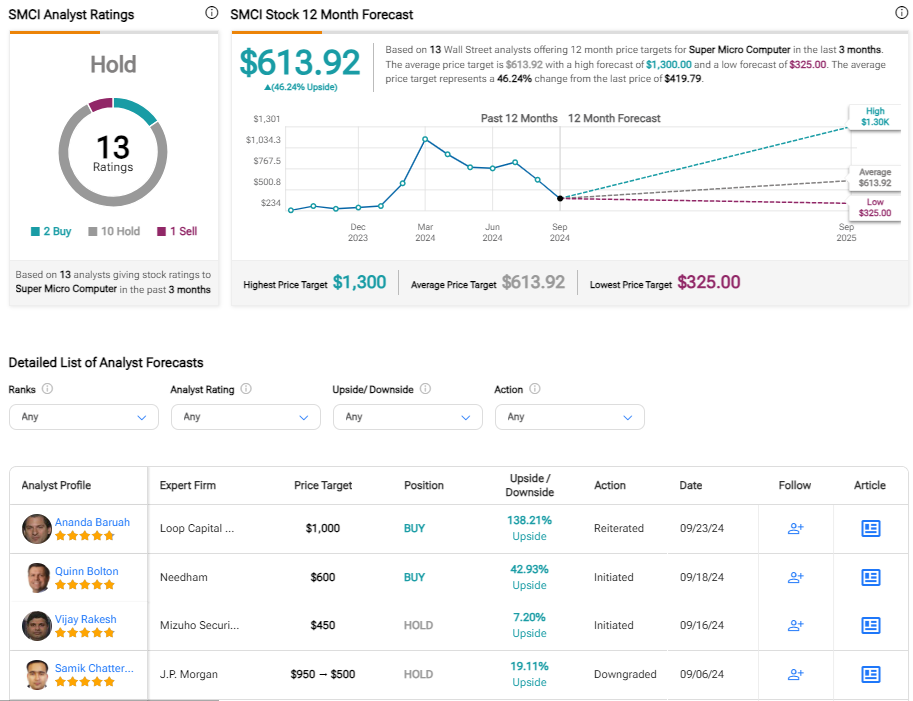

The ratings for this stock may shift quickly; however, Super Micro currently holds 2 Buy ratings, 10 Hold ratings, and 1 Sell rating from the 13 analysts covering it. The average price target for SMCI is $613.92, indicating nearly 50% upside potential. Nevertheless, it’s worth noting that various brokers may currently be reviewing their ratings for SMCI. There are low price targets of $454, $375, and $325 from CFRA, Wells Fargo (WFC), and Susquehanna, respectively. These targets were established before the DOJ investigation was publicized and may be subject to further adjustments.

The Conclusion on SMCI Stock

There’s an old saying: “You either die a hero or live long enough to become the villain.” This sentiment appears to resonate with Super Micro. The company delivered substantial profits to many investors when its stock price surpassed $1,000 per share. However, those who invested later, particularly after SMCI was added to the S&P 500, have not been as fortunate, with many posting significant losses at present. The future direction of Super Micro shares remains uncertain, hinging on investor actions amid the ongoing turbulence.

If the company’s latest financial reports hold true, SMCI shares may present an attractive opportunity now. The stock could rise swiftly if the Hindenburg report loses its impact, although predicting that outcome is challenging. I have a positive view of Super Micro’s industry and business potential related to AI, which prevents me from adopting a wholly bearish view. Thus, I maintain a neutral position here, with little expectation for SMCI shares to surpass $460 (the value prior to the DOJ probe news) without resolving the primary concerns affecting shareholder value.